-

Abc

Abc

-

Bbc

Bbc

-

Buzzfeed

-

Catalyst

Catalyst

-

Cnn

-

Drudgereport

-

Entrepreneur

-

Fastcompany

-

Fool

-

Forbes

Forbes

-

Fox

Fox

-

Futurism

Futurism

-

Gizmodo

-

Huffpost

-

Lifehacker

Lifehacker

-

Madfientist

Madfientist

-

Makeuseof

Makeuseof

-

Marketwatch

-

Menshealth

Menshealth

-

Mrmoneymustache

-

Nerdwallet

-

Nytimes

Nytimes

-

Politico

-

Producthunt

-

Reuters

Reuters

-

Salon

Salon

-

Seekingalpha

Seekingalpha

-

Shape

Shape

-

Techcrunch

Techcrunch

-

Thenextweb

-

Thepennyhoarder

Thepennyhoarder

-

Theverge

Theverge

-

Time

Time

-

Tmz

-

Vox

Vox

-

Washingtonpost

-

Wired

-

Wsj

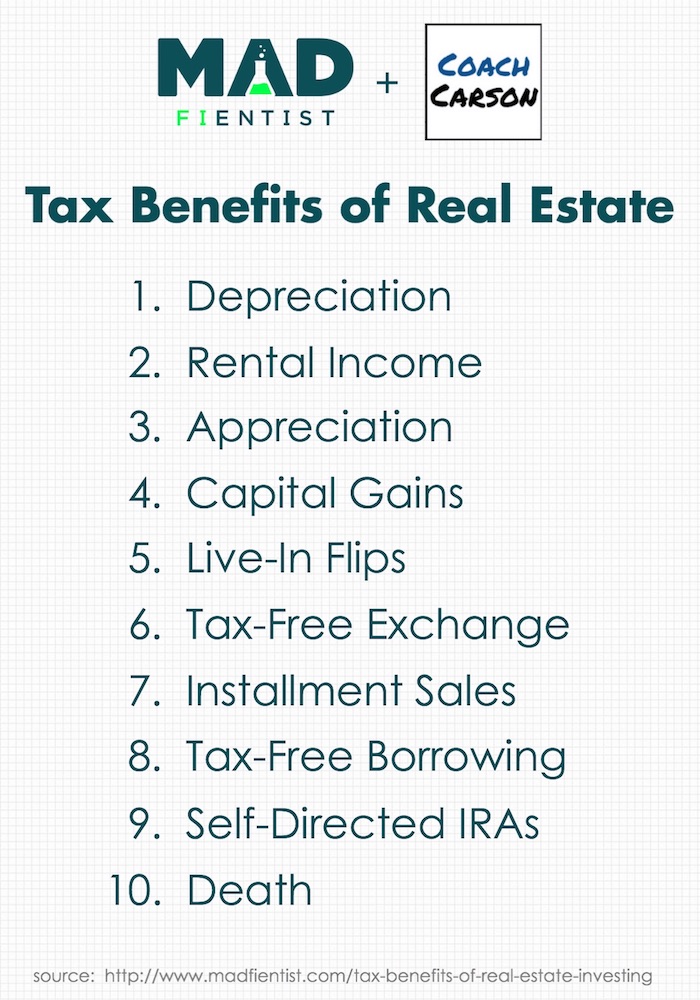

The Incredible Tax Benefits of Real Estate Investing

Today, I’m excited to share a guest post with you that was written by Chad Carson from CoachCarson.com.

This is a post I’ve been wanting to write for years but since I’m not a real-estate investor, I didn’t have the knowledge or experience to do it.

Luckily, Chad has both (he’s been a full-time real-estate investor for nearly 15 years) and was kind enough to write the ridiculously informative post you’re about to read.

Side Note: Chad’s new book, Retire Early with Real Estate, was just released yesterday and it’s fantastic so go check it out!

A big thank you to Chad for taking the time to put this together and I hope you enjoy it as much as I did!

Take it away, Coach…

The Mad Fientist is well known for dissecting and explaining amazing strategies to avoid taxes and achieve financial independence earlier. Some of my favorites are:

HSAs – The Ultimate Retirement Account Traditional vs Roth IRA How to Access Retirement Funds Early Safe Withdrawl Rates For Early Retirees

Like the Mad Fientist, I love benefiting from tax laws to help me reach financial independence earlier. But instead of pretax retirement accounts and stock index funds, my primary focus has been on the tax benefits of real estate investing.

I’d like to share 10 specific benefits with you in the rest of this article (including updates from the Tax Cuts & Jobs Act enacted by the U.S. Congress in December 2017).

But first, a little background on me.

My Real Estate Investing BackgroundI’ve been a full-time real estate investor since 2003 soon after I graduated from college. But my foray into real estate was not an obvious choice.

When my NFL football dreams fell flat (I was a middle linebacker at Clemson University), I stumbled upon the idea of real estate investing while reading a book. With a Biology degree and German minor, I was basically qualified to tell you the species of trees at a house and translate them to German! But I loved the freedom of entrepreneurship and the challenge of learning something new.

So, a business partner and I dove into real estate investing in 2003 and never looked back.

Real Estate Business vs InvestmentAs fledgling real estate investors, we had two challenges. First, we had to use real estate to make a living. Second, we had to use real estate to build wealth so that we could achieve financial independence.

To make a living we got into the real estate business. We learned how to find and quickly resell deals for a profit. Sometimes we sold these in as-is condition to other investors (aka wholesaling). Other times we fixed them up and sold them to end-users (aka retailing).

To build wealth and retire early, we also began buying real estate investments. We wanted our investments to grow and fund our early retirement with regular, steady income. Luckily, real estate has many different strategies to do both of those very well.

Along the way, we bought and sold hundreds of properties. And today we still own 90 rental units in and around the small college town of Clemson, South Carolina.

I don’t tell you this because you need to replicate what I have done. The opposite is true. If you have a regular job to pay the bills, you can accomplish amazing financial results with just a few investment properties. And the real estate strategies I have used work very well in conjunction with other investment strategies like stock index fund investing as taught by the great JL Collins.

How to Make Money in Real EstateWithout profits, tax benefits are not relevant. So, let’s first look at how you make money in real estate investing.

Just remember that real estate is an I.D.E.A.L. investment:

Income: Regular cash flow from rents or interest payments. I consistently see unleveraged returns of 5-10% from this one method of making money. With reasonable leverage, it’s possible to see these returns jump to the 10-15% range or better. Depreciation: A required accounting method that spreads the cost of an asset over multiple years (27.5 years for residential real estate). This paper expense can “shelter” or protect other income from taxes and reduce your tax bill. I’ll explain depreciation in more detail later. Equity: If you borrow money to buy a rental property, your tenant essentially pays off the property for you. You use the rent to pay the mortgage, and each month the principal paydown (aka equity) gets bigger and bigger like a forced savings account. Appreciation: Over the long-run real estate has gone up in value about the same rate as inflation (3-4%). This passive style of inflation helps, but active appreciation is even more profitable. Active appreciation happens when you force the value higher over a shorter period of time, like with a house remodel. Leverage: Many investors use debt leverage to buy real estate. This means, for example, $100,000 can buy four properties at $25,000 down instead of just one property for $100,000. Leverage magnifies the profits mentioned above (and potentially the losses). Plus, interest on debt is deductible as a business expense.

Not every real estate deal has every one of these profit centers. And sometimes you have to give up one in order to get another.

For example, one time I purchased a mobile home on land. I paid cash (so no leverage and no equity growth). The mobile home itself went down in value like a car (negative appreciation). But the income was excellent. And the depreciation sheltered some of the income from taxes.

Another investment was a more expensive single family house in a great neighborhood. Initially, the net rent after expenses barely paid the mortgage (no income). But my equity built up quickly because the loan amortized quickly. And the property was in a great location likely to appreciate at or above the overall inflation rate.

Now you know the basic ways to make money. Let’s move on to 10 different tax benefits of investing in real estate.

The Top 10 Tax Benefits of Real Estate Investing

1. Depreciation Shelters Income From TaxThe IRS uses depreciation to acknowledge that an asset wears down over time. Somehow they discovered that residential real estate wears down in exactly 27.5 years (sarcasm intended). Other assets have different timelines.

Unlike other business expenses, depreciation is a paper loss. This means you don’t spend any money, yet you still get the expense. This expense can offset taxable income and save money on your tax bill.

Here is a basic example:

Scenario #1 (without depreciation expense):

$5,000 taxable rental income x 25% federal income tax rate = $1,250 taxes owed

Scenario #2 (with depreciation expense):

$5,000 rental income – $3,000 depreciation expense = $2,000 taxable rental income

$2,000 x 25% federal income tax rate = $500 taxes owed

Tax Savings = $1,250 – $500 = $750

The higher your tax rate, the more taxes you would save in this example.

Depreciation is not unique to real estate, but real estate investing uniquely benefits from depreciation. Why? Because the cost of real estate is so large and often purchased with debt.

A $200,000 building depreciated over 27.5 years provides tax shelter of $7,272 per year. If you had 3 rental properties, you’d shelter $21,816 of income from taxes and possibly* save $5,454 on your tax bill (at a 25% rate)!

There are also other nuances and details related to applying depreciation expenses. If you want to go deep and nerd out, Depreciation For Side-Hustlers by Jeremy at GoCurryCracker.com is a great place to start. And the IRS publication about Depreciation of Rental Property makes for excellent weekend reading with a craft beer.

Also keep in mind that what the IRS giveth, the IRS taketh away. When you sell a rental property, it’s very likely that you’ll have to recapture the depreciation and pay taxes on it. The tax rate on this recaptured real estate depreciation is usually 25%. This creates a big incentive to keep real estate or to use other tax savings strategies when selling, like a 1031 exchange. I’ll discuss the 1031 exchange later in the article.

*There are catches to how much you can depreciate. I’ll cover those in the next section.

The Catch to DepreciationPrior to the Tax Reform Act of 1986 real estate investors took full advantage of depreciation and real estate losses to shelter other sources of income. This was so popular that many high-earning investors bought real estate simply for its tax advantages.

Eventually, president Reagan, congress, and the IRS caught on. So, the rules changed (this is a good lesson to not depend upon beneficial tax rules forever).

To summarize the changes, depreciation expense on a rental property was and is still deductible against other passive income. But let’s say there is an excess loss. For example, your rental income is $3,000, depreciation expense is $5,000, resulting in a $2,000 rental ( passive) loss.

Can that $2,000 loss shelter other nonpassive income, like your dividends or job income? After the tax reform, usually no.

But there are exceptions:

$25,000 exemption – You can deduct up to $25,000 of passive rental loss against nonpassive income if your income ( MAGI to be exact) is below $100,000 and you actively participate with your rental. Real estate professional – You can deduct ALL of the passive rental loss against nonpassive income if you or a spouse qualify as a real estate professional ( here are the standards). Year of sale – You can deduct ALL of the passive rental loss (even from past years) against nonpassive income the year you sell the rental property.

So, you’re good up to $25,000 of deductions if your income is below $100,000 and if you’re active with your rental. Many early retirees accomplish this anyway to benefit from other tax angles like Obamacare subsidies and Roth IRA conversion ladders.

You’re also very good if you’re a real estate professional. But among other things, the rules require you to spend 750 hours or more with your real estate activities. Sort of defeats the purpose of retirement, doesn’t it?

The third exception means you get to eventually use your passive losses when you sell. These losses can be used to offset depreciation recapture and capital gains from the sale. This is not as good as immediate deductions, but it’s a decent consolation.

Some of the other tax benefits of real estate are more straight forward.

2. Avoid FICA (Payroll) Tax on Rental IncomeJust like dividends and interest income, rental income is not subject to social security and medicare taxes (aka FICA). While this is not an enormous benefit when compared to other investments, it is significant when compared to normal earned income.

If you earn money at a normal salaried job, you pay 7.65% ( as of 2018) of your salary in FICA taxes. If you’re self-employed, you pay 15.3% towards FICA tax.

With a $100,000 salary, that’s $7,650 or $15,300 out of pocket from your salary. But if you earn $100,000 in rental income, you avoid the tax completely. This is a big incentive to start earning your money from rental income.

3. No Tax On Appreciation (aka Buy & Hold Like Buffett)One of the most tax-efficient methods to build wealth is simply not selling. Warren Buffett often says “my favorite holding period is forever.”

When you sell, you pay transaction fees, commissions, and taxes. All of these costs drag down your long-term performance because you forever lose the ability for those dollars to compound and grow.

And real estate appreciation doesn’t get taxed by the IRS. So, if you buy and hold for many years it’s possible to let your net worth grow with minimal tax exposure.

And when you do choose to sell, real estate has other benefits.

4. Capital Gains Tax at Lower RatesAs of 2018, long-term capital gains tax rates are between 0% to 20%, depending upon your tax bracket. Of course, the shifting political climate can always change these rates. But in general capital gains tax rates are lower than ordinary income tax rates.

Low capital gains rates are an advantage if you build your long-term investment strategy around strategically selling real estate for growth or living expenses.

For example, one year my deductions and rental depreciation placed me into the second lowest tax bracket. I happened to sell several properties that year, so my long-term capital gain tax rate was 0%!

But even in the higher brackets of 15% or 20%, capital gains tax would have been better than the equivalent income tax on ordinary income.

5. Live In Your Flip = No TaxesWhat if you want to avoid capital gains tax altogether? Then just buy and immediately move into the house as your principle residence. As long as you live in the home 2 out of the next 5 years, in the U.S. you can make a tax-free profit of up to $250,000 as an individual or $500,000 as a couple. Canada and the U.K. have slightly different rules, but the principle is the same.

A real estate strategy called the Live-In Flip takes advantage of this generous tax exemption. Carl from 1500days.com wrote an awesome guest post for me explaining how several live-in flips built enormous wealth and accelerated his path to early retirement.

Keep in mind that this doesn’t have to be a permanent strategy. You could do 2 or 3 flips, reinvest the earnings, and move on to other investment strategies.

6. Exchange Properties For Tax-Free GrowthAnother way to avoid capital gains tax (and also depreciation recapture tax) is a section 1031 tax-free exchange. This technique is named after section 1031 of the U.S. tax code.

A 1031 exchange allows you to trade one property for another without paying taxes. You must follow specific rules, and you must be classified as an investor (i.e. not a dealer who flips houses).

Why is this helpful? Because you get to use 100% of the profits from the sale to reinvest in the next property. This maximizes the growth and compounding of your investments.

For example, let’s say you sell a property for $300,000 without a 1031 exchange and pay $35,000 in capital gain and depreciation recapture taxes. By avoiding these taxes using a 1031 exchange, you would keep that $35,000 invested. At 10% for the next 20 years, that $35,000 would grow to over $235,000!

I am currently doing my first 1031 exchange. The technical side of the process has been relatively straightforward because I hired a third party “qualified intermediary” to handle it for me. The most difficult part has been finding a good replacement property in time, but fortunately, I do have one under contract.

Perhaps a future post can spill all of the details!

UPDATE The Tax Cut & Jobs Act of 2017 did retain the use of 1031 Tax-Free Exchanges. But there was one negative change for exchangers. Now only real property (the real estate building and land) can be exchanged. Any personal property (appliances, furniture, etc) can not be exchanged. For large apartment complexes with furnished apartments, this could mean significant taxes paid on a transaction.

7. Installment Sales For Income & Deferred TaxesThe IRS gives property investors another tool to reduce taxes on the sale of real estate. This tool is called an installment sale (aka seller financing or seller carry-back mortgage).

Like 1031 exchanges, installment sales are only available to property investors and not to dealers ( house flippers). Also like 1031 exchanges, installment sales allow an investor to defer capital gains tax, but unfortunately the entire amount of accumulated depreciation must be recaptured at the initial time of sale.

From a practical standpoint, an installment sale just means the seller of an investment property receives the sales price over time. The seller is essentially extending credit to the buyer instead of the buyer getting a bank loan ( here is my visual explanation on YouTube).

For example, a duplex owner could sell me her property for $300,000. $30,000 could be a down payment, and I would still owe $270,000 in the form of a seller financing mortgage. The terms of the financing might be $1,934 per month at 6% for 20 years.

This arrangement would be most beneficial if the duplex owner owned the property for a long time and experienced a huge run-up in prices. For example, my duplex owner might have bought the property for $50,000 over 30 years ago.

An installment sale would allow this owner to only pay taxes on the profits received each year. A $250,000 gain at one time would have pushed the seller into higher tax brackets. But the installment sale allows the seller to slowly receive the gains and possibly stay in lower, more favorable tax brackets.

It’s also worth mentioning that installment sales can be a great way to transition out of active property management and into a period of more passive income. I have done this on many properties myself.

8. Borrow Tax-Free Instead of SellTo raise cash most investors consider selling investments. As I’ve shown above, this exposes you to taxes or complicated procedures to avoid tax. But with real estate you have another choice. You can simply pull capital out of an investment tax-free by refinancing.

This is exactly what I plan to do to help fund my two daughters’ college educations. I shared all of the gory details with spreadsheets and graphs at How to Pay For College With Real Estate Investing.

In the end when I need money, I am leaning towards refinancing the properties instead of selling. This has a few benefits, including:

Get to keep a well-performing property that I know very well Benefit from future loan amortization as my tenants pay it off again Benefit from future appreciation of rents and property price NO tax paid on the cash from the refinance because it’s borrowed

You’d be right to say this technique increases my risk by incurring new debt. But as long as the debt is attractive (fixed interest, low rate, long amortization) and covered conservatively with cash flow and cash reserves, this is a risk I am personally very comfortable with given the benefits.

9. Self-Directed IRA Real Estate InvestingIRAs and 401k style retirement plans are incredible tools to build wealth while minimizing taxes. But most people think of them only as tools to invest in traditional investments like stocks, bonds, mutual funds, and REITs. While this is the norm, it’s not the rule.

The IRS does not describe what your IRA account can invest in. It only describes what you can NOT invest in. The “ do not invest list ” includes life insurance and collectibles like artwork, rugs, and antiques. Non-traditional investments like real estate, private mortgages, limited partnerships, and tax liens are therefore allowed. But most larger retirement account custodians (i.e. Vanguard, Schwab, etc) do not choose to offer them as a possibility.

So, there is an entire industry of specialized custodians who do allow investments in these non-traditional assets. A google search will give you dozens of possibilities. I personally use a company called American IRA.

While self-directed IRAs are a wonderful tool, there are many pitfalls and strict rules to be careful of. For example, you can’t self-deal by loaning money to yourself or to another disqualified person, like a close family member. If you break one of the rules, you could face large penalties and disqualification of your account from tax-free status.

My favorite way to invest with my IRA is a loan against real estate. It’s lower risk and has fewer moving parts than actually owning the real estate itself. I have also purchased local property tax liens, which often pay high interest rates and even sometimes get you a deed to real estate for pennies on the dollar.

10. Die With Real Estate (Seriously)This may sound like a joke, but one of the best plans (at least as a tax strategy!) is to die with your real estate. Instead of facing the tax issues of recaptured depreciation or capital gains tax, your heirs instead get a stepped-up basis.

For example, let’s say you bought a rental house for $100,000. Forty years later you die and the house is worth $500,000. When your heirs sell the house, they would not pay capital gains tax on the $400,000 gain. Instead, their basis would be $500,000, which means they could sell it for $500,000 and have no capital gains tax to pay.

Keep in mind that inherited assets are still subject to estate taxes. But as of this writing (2018) $11.18 million of assets are exempt from any estate taxes. So, your heirs would inherit a lot of property before paying any taxes.

Of course, you don’t have to let the tail wag the dog. Tax benefits are only part of the overall equation of finances in your life. You may have plenty of legitimate reasons (like enjoyment of life!) to pay taxes and spend the money before you die. You could also contribute a portion of your assets to charity, still pay no taxes, and help decide how worthwhile causes will benefit from your wealth while you’re alive.

Real Estate Investors Benefit From the New Tax LawNow let me cover the highlights of how the Tax Cuts & Job Acts of 2017 affected real estate investing.

After the recent U.S. tax law change, real estate investors retained almost all of the existing benefits already explained in this article. But there were some changes to pay attention to. Most will make real estate investing even more beneficial tax-wise. But a couple may negatively affect investors in certain situations.

I’ll describe the highlights of these changes below. But if you have a lot of time and enjoy punishing your brain, knock yourself out with the entire new tax law.

Personal Income Tax Rates DecreaseMost real estate investors own property personally or in an LLC (Limited Liability Corporation). Because in both instances taxes are paid on a personal (not corporate) level, the new tax law was a win with its reduced personal tax rates. Here are the new tax brackets for single and joint tax filers as of 2018:

Single Filers

Tax rate Taxable income bracket Tax owed

10% $0 to $9,525 10% of taxable income

12% $9,526 to $38,700 $952.50 plus 12% of the amount over $9,525

22% $38,701 to $82,500 $4,453.50 plus 22% of the amount over $38,700

24% $82,501 to $157,500 $14,089.50 plus 24% of the amount over $82,500

32% $157,501 to $200,000 $32,089.50 plus 32% of the amount over $157,500

35% $200,001 to $500,000 $45,689.50 plus 35% of the amount over $200,000

37% $500,001 or more $150,689.50 plus 37% of the amount over $500,000

Married Filing Jointly

Tax rate Taxable income bracket Tax owed

10% $0 to $19,050 10% of taxable income

12% $19,051 to $77,400 $1,905 plus 12% of the amount over $19,050

22% $77,401 to $165,000 $8,907 plus 22% of the amount over $77,400

24% $165,001 to $315,000 $28,179 plus 24% of the amount over $165,000

32% $315,001 to $400,000 $64,179 plus 32% of the amount over $315,000

35% $400,001 to $600,000 $91,379 plus 35% of the amount over $400,000

37% $600,001 or more $161,379 plus 37% of the amount over $600,000

Limited Itemized Deductions (Bad For High Cost Areas)

Both property taxes and mortgage interest deductions are now limited for a primary residence. But rental property taxes and mortgage interest ARE still deductible. So, this change only negatively affects owners of a primary residence in high-cost areas, like someone doing a live-in flip in San Francisco.

Mortgage interest is now only deductible on the first $750,000 of acquisition financing on primary and secondary residences. If you previously purchased a residence, a grandfather clause will allow you to continue deducting the interest on up to $1,000,000 of debt.

And state and local taxes are now limited to a total $10,000 deduction. This means, for example, that even if your total state income and property taxes (for your residence) are $20,000, you can only deduct $10,000.

20% Pass-Through Deductions (Section 199A)Perhaps the biggest new tax-break for small businesses is the 20% pass-through deduction (explained in section 199A of the new tax law). The Mad Fientist literally got the guy who wrote the book on this tax break to write an awesome guest post. I can’t hope to improve on what he already said, so I’ll be brief here.

In summary, the pass-through deduction represents a 20% reduction in taxes on your business income if you qualify! That’s huge!

But will real estate investors qualify? As far as I can tell, the answer is murky. People who flip houses should be fine. But rental property investors will need to qualify as a “trade or business,” meaning you have to engage in your business with “regularity and continuity.”

What does that mean? Even tax professionals argue about it.

But on one extreme, a very passive commercial landlord who simply collects net-lease rent checks from a Walgreens does not seem to pass the test. And on the other extreme, an Airbnb host who actively moves people in and out does seem to qualify.

Landlords in between are in the grey area.

So, I recommend you work closely with a tax professional and keep an eye on updated IRS regulations if you plan to use this deduction as a real estate investor. It could be profitable, but you need to have a good defense for your position.

Increased Depreciation (Personal Property Only)The new tax law made it easier to quickly depreciate personal property (i.e. save more on current taxes). This means your purchase of rental property equipment like carpet (unless it’s glued down), refrigerators, stoves, washers, dryers, and other non-attached property can often be 100% depreciated in the first year. You can also quickly depreciate computers and other eligible office equipment used for rentals or other business.

Creative investors and their tax professionals may also use cost segregation (ie. splitting up the basis of a rental into separate components) to also write off land improvements. This means things like sidewalks, driveways, and landscaping which could be depreciated more quickly.

But this area of tax law is another tricky one. Tread carefully and get professional tax help.

And if you read tortuous (yet sometimes humorous) tax articles for fun (Mad Fientist, GoCurryCracker, and I are raising our hands, anyone else?), then have fun reading my favorite tax geek in this Forbes article Changes to Depreciation in the Tax Law.

Opportunity ZonesA new concept called an “ Opportunity Zone ” is perhaps the most innovative and profitable tax law change for real estate investors who can take advantage of it.

To benefit from the change, you must invest in certain areas of the country that are designated as Opportunity Zones. These zones are typically economically-distressed areas ( national map of all economic zones).

The vehicle for this investment is called an Opportunity Fund, which is just any partnership or corporation that self-certifies that it is an Opportunity Fund (i.e. you just fill out an IRS form).

How exactly do real estate investors benefit? Here’s an explanation of three primary ways that I learned from the Economic Innovation Group, who has followed the rollout of opportunity zones closely:

1. A temporary deferral of capital gains taxes if funds are invested in an Opportunity Fund. You eventually pay taxes on the deferred gain either when the opportunity zone investment is sold or December 31, 2026, whichever is earlier.

For example, you could sell $200,000 of appreciated stock (i.e. a basis of $100,000), reinvest in an opportunity fund, and pay no taxes on your $100,000 of gain until the fund’s property is sold or December 31st, 2026.

That’s years of tax-free compounding!

2. A step-up in basis for capital gains reinvested in an Opportunity Fund. The basis is increased by 10% if the investment in the Opportunity Fund is held by the taxpayer for at least 5 years and by an additional 5% if held for at least 7 years, thereby excluding up to 15% of the original gain from taxation.

So, in addition to the deferral of tax in #1, you get a reduction of your original taxable gain by holding onto the investment for 5 to 7 years or more.

3. A permanent exclusion of your taxable capital gains from the sale or exchange of an investment in an Opportunity Fund if the investment is held for at least 10 years. This exclusion only applies to gains accrued after an investment in an Opportunity Fund.

For example, if you bought an Opportunity Zone property for $200,000 and sold it more than 10 years later for $500,000, you’d pay zero tax on $300,000 of new capital gain!

As you can see, this is an incredibly generous tax benefit. But it’s such a new provision that the method of implementation and long-term effects are unknown.

I plan to keep a close eye on it, so perhaps the Mad Fientist and I can brew up a future article to keep you updated!

ConclusionAs you have seen, tax benefits are a compelling reason to get involved in real estate. But tax benefits are never the sole reason to invest in real estate or anything else. Basic economics and quality of your investments are primary factors to consider when choosing your strategy.

And you also need to make sure real estate fits your lifestyle. I think real estate is often overlooked as a viable retirement strategy, especially by early retirees. But it’s clearly not for everyone. Do your homework and figure out what’s best for you.

And if you choose to invest in real estate, be sure to build a team of professionals to support you. One of the most important team members will be a tax professional like a CPA or qualified tax attorney. All of the strategies I’ve mentioned here are a start, but a professional can help you apply the details to your situation.

What do you think? Have you benefited from investing in real estate? What tax angles have been most beneficial to you? Did I leave any out?

Hey, it’s the Mad Fientist again.

That was amazing, wasn’t it?

If this post got you excited about real estate and you’re interested in learning how you can use real estate to retire early, Chad just published a book that dives into exactly that topic – Retire Early with Real Estate!

I’ve also interviewed Chad twice for the Financial Independence Podcast so check out this episode to hear more about Chad’s personal story and real-estate investing experience and listen to this episode to discover some of the best real-estate-investing strategies you can use on your journey to financial independence!

Chad has a podcast of his own and he just released an episode about the tax benefits of real-estate investing so check that out here to go even deeper into this topic.

Finally, make sure you head over to his site to say hello and to check out all the great stuff he’s got going on over there!

Related Post Afford Anything - Dive Into Real Estate Investing

Paula from AffordAnything.com joined me to discuss how she’s using real estate investing to achieve early financial independence!

The post The Incredible Tax Benefits of Real Estate Investing appeared first on Mad Fientist.