-

Abc

Abc

-

Bbc

Bbc

-

Buzzfeed

-

Catalyst

Catalyst

-

Cnn

-

Drudgereport

-

Entrepreneur

-

Fastcompany

-

Fool

-

Forbes

Forbes

-

Fox

Fox

-

Futurism

Futurism

-

Gizmodo

-

Huffpost

-

Lifehacker

Lifehacker

-

Madfientist

Madfientist

-

Makeuseof

Makeuseof

-

Marketwatch

-

Menshealth

Menshealth

-

Mrmoneymustache

-

Nerdwallet

-

Nytimes

Nytimes

-

Politico

-

Producthunt

-

Reuters

Reuters

-

Salon

Salon

-

Seekingalpha

Seekingalpha

-

Shape

Shape

-

Techcrunch

Techcrunch

-

Thenextweb

-

Thepennyhoarder

Thepennyhoarder

-

Theverge

Theverge

-

Time

Time

-

Tmz

-

Vox

Vox

-

Washingtonpost

-

Wired

-

Wsj

The Real Benefit of Being Rich

There have been a lot of big bills coming across my kitchen table recently. Property taxes, car registrations, income taxes, things for the school orchestra in which little MM plays the standup bass. Plus the usual credit card bills for all my spending on groceries and not-all-that-rare luxury indulgences. There’s nothing bad or unexpected in this pile of bills, but I still see it adding up to a tidy sum.

There have been a lot of big bills coming across my kitchen table recently. Property taxes, car registrations, income taxes, things for the school orchestra in which little MM plays the standup bass. Plus the usual credit card bills for all my spending on groceries and not-all-that-rare luxury indulgences. There’s nothing bad or unexpected in this pile of bills, but I still see it adding up to a tidy sum.

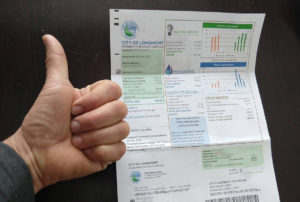

But this morning as I was looking at the latest one – a bill from the City of Longmont for all the various utilities, I noticed that the same familiar feeling crept across my chest that I had felt for all of these other expenses: a feeling of warmth and reassurance.

The utility bill had a little note on it that said “DON’T PAY – account is being paid by credit card.”

So I can be reassured that whenever the due date comes up, the right amount of money will be sucked out of my credit card account to pay for the electricity and gas and water and trash service. And then whenever that credit card bill is due, another automatic payment will suck the right amount of money out of my checking account, and I’ll remain debt free.

Isn’t this remarkable? I get to frolic around in this super comfortable house of mine, keeping it warm in winter and flipping on lights and stereos and pulling cold beers out of the fridge and hopping into a hot shower whenever I like. Hosting guests and sharing the fresh food and hot showers and cold beers with them too.

Music and movies stream in over the fiber optic internet connection, and my fleet of crisp and well maintained bikes flow in and out of the garage doors in the back without a second thought about how the bills will be paid. In fact, I don’t even know when a single one of my due dates hits during the month, and I also don’t keep track of when my dividends or payments come in from stock investments or my little one-owner business.

Everything is worry free, because I know there’s enough, and the very feeling of knowing that I have enough warms my heart and soul every single day. It is a feeling of liberation and freedom and a glider that keeps me soaring high above the bullshit of worry or having to sell out my free time for activities that aren’t really helping anyone. To me, this feeling is the very core of being a Rich Person.

But now that I’ve got you imagining a glossy and pampered douchebag, barking orders at my live-in assistant and personal stylists before I climb into a white-leather Lexus to roll down to the marina, I should mention a few additional details.

All this incredible luxury occurs within my small house on the train tracks, tucked into a less-than-gentrified neighborhood at the corner of a less-than-world-class city. When I sit at that kitchen table, I gaze out at a shitty pergola structure that really needs the first available appointment with my fire pit, which covers a sadly undersized side patio, which is currently the only outdoor living space on my postage stamp sized lot.

When I ride those wonderful bikes out of that tidy garage, I pedal past my 21-year-old Honda Odyssey, and I’m usually en route to Sam’s Club to pick up another backpack load of discount groceries, or to perform another few hours of dirty manual labor at my always-under-construction coworking space downtown. My flannel shirt may have holes in its sleeves from welding sparks and my jeans may have a ripped seam or two from performing squats without proper workout gear.

The two stories above are two different takes on the exact same life. As a high income professional, you might have shuddered at the second one. Riding a bike during Colorado’s unpredictable snowstorms or searing desert heat, eating at restaurants less than once a month, cutting your own hair, or standing atop a 32 foot ladder to reach the last patch of your house with a paintbrush are surely just the desperate acts of an extremely frugal man, who does them to save money because he needed to escape the corporate world, right?

But unfortunately for my uneasy high income critics, this is just not true. Because of my advancing age, natural growth of the stock market, and ongoing love for work including writing this blog, I can afford to not do any of these things. In fact, depending on how you measure it, last year I spent only about 5% of my income on myself. I could spend twenty times more and still not even have to go back and get a real job!

At the same time, I have a few acquaintances – perfectly wonderful and thoughtful people – who do spend twenty times more and are still struggling to pay the bills and work one last year to get ahead of the treadmill. And they compare themselves to their other CEO peers, noting with relief that at least they spend far less than those crazy spenders and thus are living sensible lives.

Who is the reasonable one here, and who is off with their heads in the clouds? Mr. Money Mustache, or Corporate Chief Christine?

The answer of course is that we are both floating in space. My lifestyle is less expensive, but it’s still way more than almost anyone gets to experience, even in the richest country in the world. A single man in a three bedroom house worth over $350,000, with a seven passenger racing sofa parked out back that can tow 1.5 tons of construction materials in his cargo trailer, both of which he only needs once or twice per month. Plane tickets and parties, nice clothes and Amazon deliveries. It is all stuff that my teenaged self could have never even imagined.

So I could spend more, but I could also spend less, and I could be just as happy at any of those levels. My spending level today is just the result of my own imperfect efforts to build the happiest life I can manage while wasting as little as I can without being overly inconvenienced. And hopefully so is yours.

The trick is in realizing you can always go further while also ending up happier in the process. In not being afraid to add challenge to your life, because the right kind of challenge is a win/win rather than a tradeoff. And to not worry about what experiences you might be missing, but being mindful of the beauty of whatever you are doing right now.

At almost every moment in time, there is always something you could be doing that costs absolutely nothing, but which also makes you absolutely happy.

Your lifetime wealth surplus depends on how often you choose to find these joyful moments.

And only when you go far enough so that your spending is only a small portion of your income, do you become rich. It is at this point that your incoming bills feel like a joy rather than a burden, and your children’s future educations feel like a playground rather than a minefield. Even lurking medical expenses or aging parents who may need your help or the inevitable blow-ups in the economy just become things you are prepared for, but not worried about.

Right now, if you have any sort of income at all, it is probably enough to make you feel rich. The only question is, what changes do you need to make to your life over the next few months to unlock this joyful feeling?